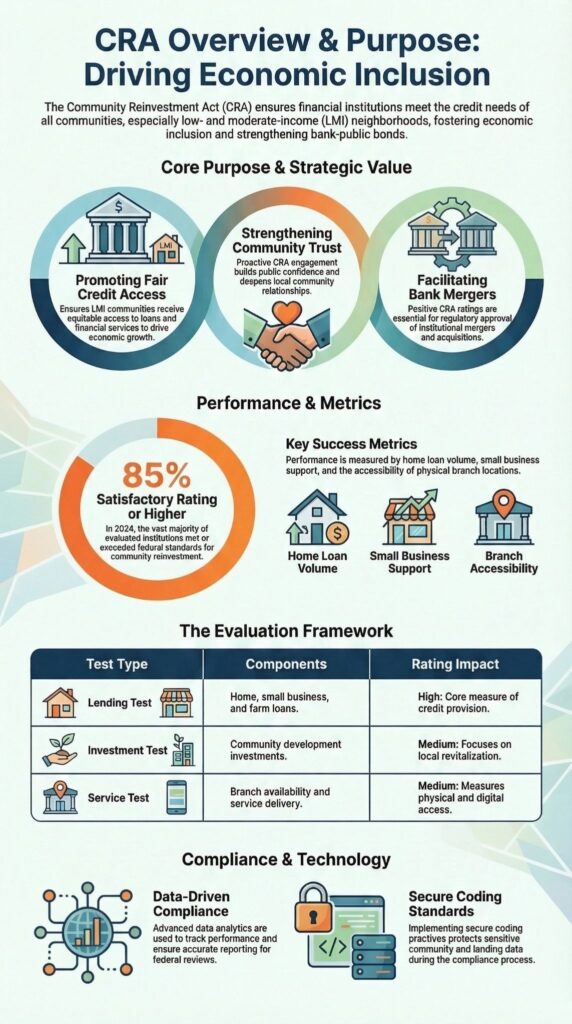

The CRA overview & purpose centers on ensuring that U.S. banks and thrifts meet the credit needs of all communities, particularly low- and moderate-income (LMI) neighborhoods, while maintaining safe banking practices.

Enacted in 1977, the Community Reinvestment Act addresses discriminatory lending practices like redlining and encourages financial institutions to balance profitability with social responsibility.

In our experience, combining data analytics, compliance frameworks, and secure operational practices helps banks achieve these goals effectively. Understanding the CRA’s objectives and practical implications is essential for banks, regulators, and community advocates. Keep reading to explore how the CRA continues to shape inclusive lending today.

Quick Wins for CRA Impact

The Community Reinvestment Act (CRA) guides banks to support low- and moderate-income communities while maintaining safe banking practices. Key areas to focus on include:

- Responsive lending: Providing fair access to credit in LMI communities.

- Regulatory evaluation: Performance assessed by the Federal Reserve, FDIC, and OCC through lending, investment, and service tests.

- Strategic influence: Strong CRA performance affects mergers, branch approvals, and builds community trust, promoting financial inclusion.

What is the EU Cyber Resilience Act

The CRA overview highlights the need for financial institutions to address the credit needs of all communities, especially low- and moderate-income (LMI) areas, while adhering to EU Cyber Resilience Act standards for secure practices.

As highlighted by European Journal of Risk Regulation

“The Cyber Resilience Act… entered into force Regulation (EU) 2024/2847 … on horizontal cybersecurity requirements for products with digital elements.” – European Journal of Risk Regulation

While banks, savings associations, and certain thrifts are the primary focus, we’ve observed that robust internal systems and secure coding practices play a crucial role in tracking performance and ensuring compliance.

Key CRA components include:

- Lending tests – Evaluating home loans, small business lending, and community development financing in LMI neighborhoods

- Investment tests – Assessing qualified investments and contributions to local projects that support underserved populations

- Service tests – Reviewing branch locations, hours of operation, and accessibility for all customers

In our bootcamp, we emphasize applying secure coding practices to CRA data systems. Ensuring accurate geographic assessments and loan origination tracking not only improves regulatory alignment but also reinforces transparency, giving teams confidence that their systems support both compliance and community-focused objectives.

EU Cyber Resilience Act explained

The primary purpose of the CRA is to prevent redlining and discriminatory lending while encouraging financial institutions to invest in low- and moderate-income (LMI) communities, aligning with principles outlined in EU Cyber Resilience Act explained.

In our experience, tracking credit needs and monitoring lending trends allows banks to support economic development, affordable housing, and small business growth effectively. Secure internal systems help ensure that data collection is accurate and consistent, supporting both compliance and meaningful community impact.

The CRA promotes financial inclusion by requiring proactive community development. Key requirements we emphasize in training include:

- Monitoring minority deposits and lending to prevent systemic exclusion

- Aligning services with local demographics and income distribution

- Performing needs-based lending that reflects community requirements

During CRA evaluations, regulators review borrower distribution, geographic coverage, and qualified investment portfolios. Banks that fall short may receive “needs improvement” or substantial noncompliance ratings, triggering mandatory remediation plans. We teach teams to follow best practices such as:

- Careful data collection and HMDA integration

- Reviewing public comments on lending and community development

- Maintaining accurate records of investments and loans

By embedding these practices, institutions can meet CRA objectives while ensuring transparent, community-focused lending.

EU Cyber Resilience Act summary

While the CRA’s objectives are clear, putting them into practice often presents challenges for banks and thrifts, particularly in light of the EU Cyber Resilience Act summary on regulatory compliance.

From our experience, institutions frequently struggle with defining geographic boundaries, identifying underserved markets, and balancing profitability with community responsibilities. Secure internal systems and coding practices play a critical role in addressing these challenges and ensuring accurate reporting.

We focus on three practical areas to strengthen CRA implementation:

- Digital delivery systems – Ensure mobile banking and online loan applications are inclusive for low- and moderate-income households

- Data analytics – Use mapping, geocoding, and CRA-specific software to assess assessment area demographics accurately

- Community engagement – Conduct public meetings, issue CRA notices, and participate in local initiatives to stay informed about evolving credit needs

Key CRA evaluation components and metrics include:

| Component | Key metrics | Regulatory source | Typical rating impact |

| Lending tests | Home loans, small business loans, community development loans | FDIC CRA | Satisfactory / Outstanding |

| Investment tests | Qualified investments, community projects | Federal Reserve CRA | Satisfactory / Outstanding |

| Service tests | Branch distribution, hours, mobile access | OCC CRA | Satisfactory / Outstanding |

From our hands-on experience, prioritizing secure coding practices in loan origination systems and public data management reduces reporting errors and improves responsiveness to underserved communities.

Why Cyber Resilience Act matters

From the perspective of CRA officers and compliance teams, the law provides both guidance and insights on why the Cyber Resilience Act matters. In our experience, banks that develop structured strategic plans, conduct regular internal audits, and implement targeted training programs maintain stronger CRA ratings and navigate regulatory expectations more smoothly.

Key areas we emphasize in training include:

- Policy updates – Continuously reviewing lending strategies to stay aligned with CRA modernization efforts

- Performance context factors – Considering asset-size thresholds, peer comparisons, and innovation scores during evaluations

- Voluntary commitments – Supporting philanthropic initiatives, impact investing, and community development loans to demonstrate proactive engagement

We’ve observed that banks integrating secure coding practices into their data collection systems gain clearer insights into retail lending distribution, minority deposits, and CRA hotspots.

Embedding security in these systems reduces reporting errors and allows teams to respond more quickly to compliance inquiries. For us, combining secure coding with strategic CRA planning not only streamlines audits but also strengthens the institution’s ability to serve underserved communities effectively.

Cyber Resilience Act software impact

Certain edge cases make CRA applicability more complex, including rural markets, digital-only banks, and alternative data sources for credit assessments.

Insights from International Cybersecurity Law Review indicate

“The CRA introduces mandatory ‘secure by design’ requirements and lifecycle security obligations with respect to hardware and software products.” – International Cybersecurity Law Review

From our experience running a secure development bootcamp, we’ve seen that transparency is critical in these scenarios. Regulators rely on public file disclosures, CRA protests, and intervener status procedures to ensure fairness, even when lending practices fall outside conventional models.

Software plays a central role in managing CRA compliance across different contexts, especially following the Cyber Resilience Act software impact guidelines for secure systems.

- Statewide evaluation – Rural and metropolitan markets require tailored assessment methodologies to reflect local needs accurately

- Merger approvals – CRA performance can influence board decisions on expansions and acquisitions

- Responsive lending – Needs-based loans and community development initiatives remain core to CRA compliance

In our training, we emphasize that building secure, reliable systems not only meets regulatory expectations but also empowers institutions to respond proactively to evolving market and community demands, ensuring that underserved populations receive fair and timely access to credit.

Cyber Resilience Act overview for developers

Credits : NCRC

CRA modernization, including proposals in the 2025 updates, highlights digital access, data analytics, and equitable investment, which developers can implement effectively using Cyber Resilience Act overview for developers practices.

From our experience training secure development teams, understanding these updates helps developers design systems that support fair lending while meeting evolving regulatory requirements.

Regulators aim to simplify asset-size thresholds, retail service coverage, and innovation assessments, but maintaining compliance with fair lending standards remains essential.

Key areas we focus on in training include:

- HMDA integration – Enhances tracking of home improvement loans, multifamily dwellings, and small business lending

- Digital delivery systems – Ensures mobile banking access reaches underserved markets, improving transparency and accessibility

- Regulatory reform – Aligns CRA expectations with emerging fintech partnerships and competition from non-bank lenders

We’ve found that embedding secure coding practices in CRA-related software enables accurate data collection and reliable reporting.

Teams that adopt these practices early can streamline compliance, monitor underserved lending patterns effectively, and support equitable community investment. In our bootcamp, we emphasize hands-on exercises that teach developers how to integrate these principles into real-world systems, ensuring both regulatory alignment and meaningful community impact.

FAQ

What is the main goal of the Community Reinvestment Act (CRA) overview?

The CRA overview explains the law’s purpose to encourage banks and thrift institutions to meet the credit needs of low- and moderate-income (LMI) communities.

It highlights key elements such as community development, affordable housing loans, small business lending, and needs-based lending. Understanding the CRA overview helps stakeholders evaluate CRA performance, track reinvestment obligations, and prevent discriminatory lending while promoting economic inclusion.

How does the CRA purpose prevent redlining in moderate-income neighborhoods?

The CRA purpose ensures banks provide fair access to credit in underserved areas. Through lending tests, investment tests, and service tests, institutions identify gaps in LMI communities.

CRA ratings, public comments, and regulatory exams promote safe banking practices and help prevent redlining. This framework encourages equitable credit distribution, supports underserved markets, and strengthens community development in moderate-income neighborhoods.

What are CRA evaluation metrics for banks and thrift institutions?

CRA evaluation metrics measure how well banks meet community credit needs. Regulators, including the Federal Reserve CRA, FDIC CRA, and OCC CRA, use supervisory guidance, regulatory exams, and public data portals to assess community development loans, qualified investments, retail lending distribution, and responsiveness to local credit needs.

Ratings can be outstanding, satisfactory, needs improvement, or substantial noncompliance, based on borrower distribution and geographic assessment areas.

How can the public participate in CRA performance reviews?

The public can participate by submitting comments, attending public meetings, or filing CRA protests. Agencies maintain public files and post CRA notices online to ensure transparency.

Citizens can use mapping tools, track branch openings, and monitor retail services and lending trends. Public input influences policy updates, supervisory guidance, and CRA modernization efforts, enhancing community development, economic inclusion, and fair lending practices.

What updates are expected under CRA modernization and 2025 CRA updates?

CRA modernization focuses on improving data collection, HMDA integration, and digital delivery systems, including mobile banking and online loan applications. Updates also address branch distribution, de minimis lending, and alternative data sources to better evaluate LMI communities.

The 2025 CRA updates aim to refine supervisory criteria, performance metrics, and measurable outcomes, ensuring needs-based lending, financial inclusion, and equitable credit access in metropolitan and rural markets.

Take Control of CRA Compliance

Keeping up with CRA requirements while driving meaningful community impact can feel complicated and slow. You might struggle to balance regulatory needs with practical implementation. Waiting only makes compliance harder and opportunities smaller.

Secure Coding Practices offers hands-on training to help your team build secure, compliant processes efficiently. Their bootcamp provides practical skills, SDL guidance, and real-world exercises so banks can confidently implement CRA strategies, improve compliance ratings, and support underserved communities without guesswork.

References

- https://doi.org/10.1017/err.2025.9

- https://link.springer.com/article/10.1365/s43439-025-00162-4

Related Articles

- https://securecodingpractices.com/eu-cyber-resilience-act-for-secure-coding-practices/

- https://securecodingpractices.com/what-is-eu-cyber-resilience-act/

- https://securecodingpractices.com/eu-cyber-resilience-act-explained/

- https://securecodingpractices.com/eu-cyber-resilience-act-summary/

- https://securecodingpractices.com/why-cyber-resilience-act-matters/

- https://securecodingpractices.com/cyber-resilience-act-software-impact/

- https://securecodingpractices.com/cyber-resilience-act-overview-developers/